First, I have to make it undeniably clear that I am no finance wiz…

The only math courses I took in college were statistics (twice) & a family finance class. I’ve also read one of Dave Ramsey’s books…that’s it. The extent of my financial knowledge is relatively limited.

However, I’m 23 years old, married, and my husband and I are completely financially independent.

We rent a 1 bed/1 bath apartment near Salt Lake City, we have a car payment, we give 10% of our income to our church as tithes, and we pay $1000 a month towards my student loans so that they will be paid off within the next year. Thankfully, we have $0 in credit card or other debts and we have invested and saved a little bit on the side.

We both work normal hour, full time jobs and we still get to have some fun and eat at good restaurants.

BUT, none of that would be possible without a budget.

I live and breathe our budget.

I check our bank accounts pretty much everyday, even if we haven’t purchased anything, solely for the purpose of knowing where we stand financially. I evaluate all of our expenses monthly, while factoring in any potential new expenses, and then I alter the categories & allotments in our budget as needed.

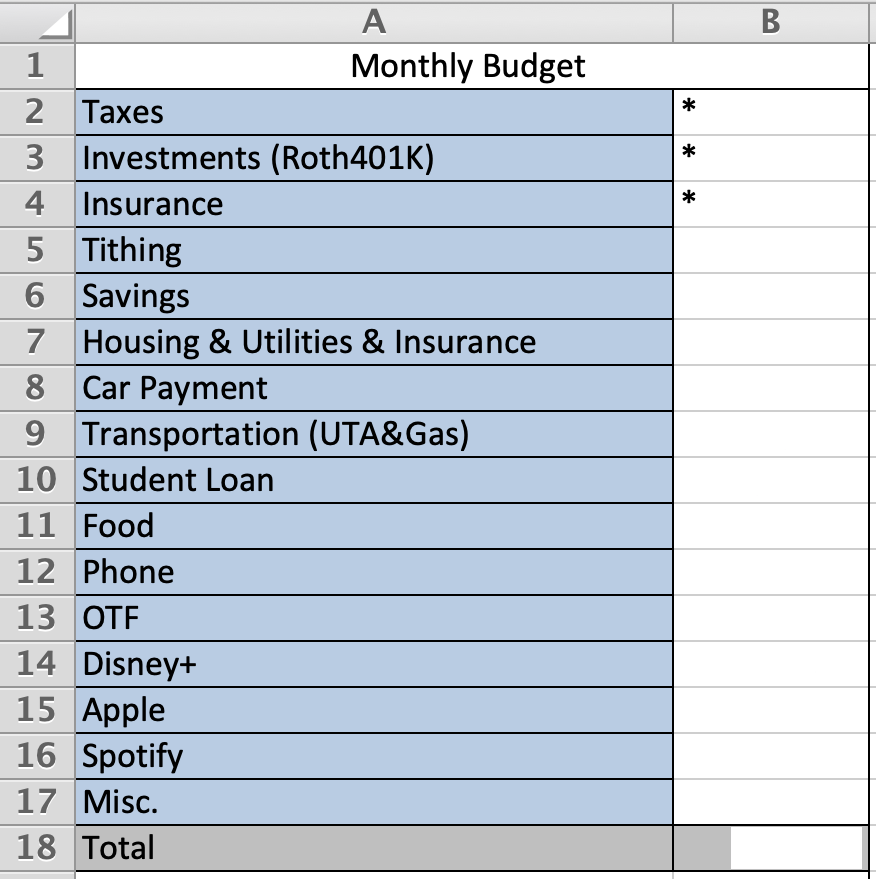

Here’s how I do it:

- I start with a basic spreadsheet.

- I list every single one of our monthly expenses – even if it’s only $5 – I like to see everything.

- Then, I calculate our monthly income – Sean and I are both on a bi-weekly pay schedule – so I look at our bank account – take each of our paycheck deposit amounts – multiply it by 2 (for twice a month) & add them together to get our combined total.

- I then auto-sum columns B2-17 so that they will automatically add and fill B18 – my monthly total – which in the end should equal the amount that I calculated previously.

- I then start to fill in each category…

The categories marked with * are those that are removed before we even receive our paychecks & are not included in the monthly total.

I typically fill in our categories like this…

- Tithing – top priority for us – 10% – it gets paid before anything else – it is also easy to calculate and the amount does not change much from month to month.

- Housing & Utilities & Renter’s Insurance – our 2nd priority – again, these amounts do not change from month to month – other than our utility amounts that fluctuate with the seasons by a few dollars here and there.

- Car payment – another essential payment that is the same every month – catching the trend – static amounts come first – they don’t change so they are the easiest to fill in first.

- Other payments that fall in the static category – Phone bill, my Orange Theory membership, and entertainment platforms like Disney, Apple, & Spotify. They are easy to fill in, then I move on.

Next I move to the trickier amounts – these are completely subjective, they can change from month to month & it is up to me to decide how much to allot for each.

- Student Loan – this is something we are hustling to get rid of. We have chosen to allot $1000 a month to pay off this loan so that it can go away. The minimum monthly payment is much, much less, but we choose to pay more.

- Transportation Costs – Sean typically takes a train to work – he hops on at the station right across the street from our apartment and it takes him pretty much all the way to his office, which is about 30 minutes south and even longer during rush hour. The train takes a little bit longer but this way, we save on gas & he avoids awful Utah drivers…I mean traffic. I thankfully work 10 minutes down the road from our apartment so I take the car and barely use any gas. The train fees are static but the amount we allot for gas changes, depending on where we choose to go. Hint: we don’t spend that much on gas so this allotment is low.

- Food – this is the hardest part of our budget – one of our favorite hobbies as a couple is going out to eat. Don’t get me wrong, I like to cook and try new recipes, but sometimes it is just easier & more fun to go out. Our food budget accounts for groceries & restaurants combined – depending on the month, the amounts for each change. Compared to our other expenses that are mostly static and easy to stay within budget on, this category is a work in progress & in the beginning, felt like a total guessing game.

- Savings – this is a tricky one too – if you are a die hard Dave Ramsey fan you would know that technically we are not even supposed to have this as part of our budget due to the fact the we are still making both student loan & car payments (he likes you to throw all of your $$$ at those debts before you save)…however, I like to be prepared for anything, so we still save a little.

- Lastly, a miscellaneous category, this is however much is leftover after all of our other expenses – typically just a couple hundred dollars that ends up being spent on more food…that’s pretty much all we buy, can anyone else relate?

And that’s it my friends. A basic budget to keep you sane.

Other helpful tools include Dave Ramsey’s books, website, & Instagram page (@daveramsey) – can you tell that I love that guy?

We also use the Mint app – just sync all of your accounts and it will categorize all of your expenses for you and tell you how much money you are really spending – the food amount shocks me every time…we’re working on it.

Again, a budget is just a way for you to be in control & know exactly where your money is going. It can show you where you need to cut back or maybe where you can even spare to spend a little more. It is fantastic for planning out how you are going to eliminate debt or for achieving financial goals, like saving for a home or vacation.

I absolutely recommend, and I think our pal Dave would too…

Happy Budgeting!